{kind=link}

01

2007-2016

Interface layer

Mobile, sensors and app distribution

Smartphones normalized cameras, GPS, IMUs, payments, maps, notifications and app stores. Robots and agents inherit this world of cheap sensors and software distribution.

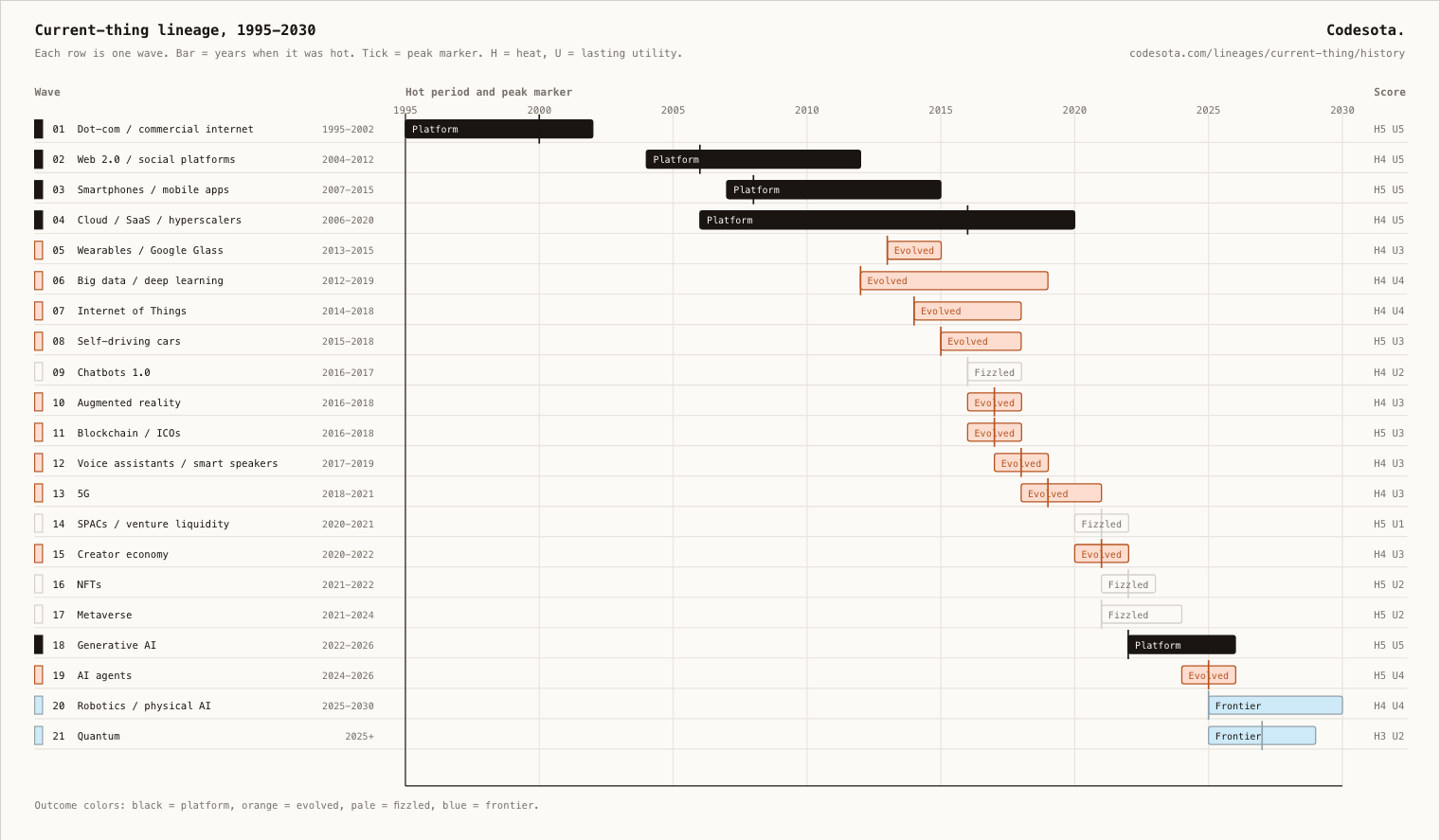

This is the dated lineage behind the phrase "the current thing": not just which technology was mentioned, but when attention peaked, what evidence made it feel real, and whether it became infrastructure or only a story.

How intense the attention cycle was at or near peak.

How much repeatable infrastructure or workflow value survived.

Platform means the wave became substrate; evolved means a narrower real layer; fizzled means the broad thesis failed.

Agents sit above software tools. Robotics sits above hardware, sensors, control loops and regulated environments. The serious lineage is the stack below them: cloud, GPUs, perception, simulation, fleet software, drones, warehouses and industrial automation.

Smartphones normalized cameras, GPS, IMUs, payments, maps, notifications and app stores. Robots and agents inherit this world of cheap sensors and software distribution.

Elastic compute, object storage, GPU training, telemetry and MLOps made it practical to train models, serve them, monitor them and improve them continuously.

Computer vision, speech, reinforcement learning, synthetic data and simulation made machines better at reading messy environments before acting inside them.

The real physical-ai base is not humanoid demos. It is repeatable work in bounded environments: factories, logistics, inspection, agriculture, labs and delivery routes.

Language and vision-language models become planners, translators and interfaces between humans, software tools and physical systems.

Every company would become an internet company.

Web access, browsers, online retail, portals and venture-backed dot-com IPOs made the internet feel like a new economy.

Nasdaq peaked on March 10, 2000 at roughly 5,048 before falling sharply through October 2002.

Search, e-commerce, online advertising, SaaS distribution, web-native media.

Most thin dot-com retailers, portals with no durable moat, growth-at-any-price valuations.

Users would create the web, and social graphs would organize attention.

Facebook, YouTube, Twitter, user-generated content, RSS, blogs and social feeds moved the web from pages to participation.

The mid-2000s produced the dominant consumer internet platforms that later became default distribution channels.

Social feeds, creator platforms, identity graphs, viral distribution, influencer media.

Most generic social networks, blog networks, check-in apps and user-generated-content clones.

The internet would move into pockets, cameras, maps and app stores.

The iPhone arrived in 2007; the App Store followed in July 2008 and turned mobile into a developer and distribution platform.

Apple announced 10 million App Store downloads in the first launch weekend in July 2008.

App stores, mobile commerce, ride-hailing, delivery, maps, mobile-first social, camera-native products.

Most branded apps, QR gimmicks, weak location-based social apps, tablet-first publishing fantasies.

Compute would become an elastic utility and software would move to subscriptions.

AWS EC2 launched in 2006, then cloud shifted from startup infrastructure into enterprise procurement and platform strategy.

In 2016 Gartner said cloud shift would affect more than $1 trillion in IT spending by 2020.

AWS, Azure, Google Cloud, SaaS, DevOps, serverless, data platforms, usage-based software.

Private-cloud cargo culting, lift-and-shift without governance, many PaaS-only bets.

Computing would move from pockets onto faces, wrists and bodies.

Google Glass, Pebble, fitness bands and smartwatch rumors made wearables feel like the next post-phone interface.

Google Glass Explorer Edition reached early users in 2013 at $1,500, then Google ended the Explorer sales program in January 2015.

Apple Watch, fitness trackers, health sensors, enterprise assisted-reality niches, earbuds as computers.

Consumer smart glasses as a mass 2010s platform, always-on face cameras, Glass-style social behavior.

Data plus GPUs would let software learn instead of being hand-coded.

Deep learning broke through in vision, speech and translation while companies built data lakes and ML teams.

AlexNet's 2012 ImageNet result became the symbolic deep-learning trigger for modern AI investment.

GPU training, embeddings, recommendation, computer vision, speech recognition, MLOps.

Data lake projects without product loops, Hadoop maximalism, vague AI transformation programs.

Every object would become connected, instrumented and programmable.

Cheap sensors, cloud telemetry, smartphones and industrial digitization made connected devices feel like the next platform after mobile.

Gartner's 2014 hype-cycle discussion put the Internet of Things at the Peak of Inflated Expectations.

Industrial IoT, telemetry, smart meters, fleet monitoring, connected appliances, edge gateways.

Smart-fridge theater, insecure consumer gadgets, generic IoT platforms without domain workflows.

Autonomous vehicles would soon replace human driving and car ownership.

Tesla Autopilot, Google/Waymo progress, Uber's autonomy push and GPU perception made autonomy look close.

Fortune described autonomous vehicles as Gartner's most hyped emerging technology of 2015.

Waymo-style geofenced robotaxis, ADAS, autonomous trucking pilots, perception stacks, mapping and simulation.

Near-term everywhere autonomy, fast elimination of car ownership, many lidar/AV SPAC stories.

Messaging bots would replace apps and become the new business interface.

Facebook opened Messenger to bots, brands rushed in, and conversational commerce looked like the next app store.

TechCrunch wrote at launch that chatbots had suddenly become the biggest thing in tech; Facebook later said the launch was overhyped.

Support automation, notification flows, conversational UX patterns, bot frameworks, early agent lessons.

Menu-driven Messenger bots as app replacements, brittle natural-language commerce, bot-store dreams.

Phones and glasses would overlay digital objects onto the physical world.

Pokemon Go proved mass AR attention, then Apple ARKit and Google ARCore made mobile AR a developer platform.

TechCrunch reported more than 13 million ARKit-only app downloads after iOS 11 launched in September 2017.

Camera effects, visual search, AR try-on, spatial mapping, industrial overlays, mixed-reality components.

AR apps as a standalone app-store category, everyday phone AR layers, many location-AR clones.

Tokens would decentralize finance, computing, storage, governance and the internet itself.

Ethereum smart contracts made token launches easy, Bitcoin price attention pulled retail capital in, and ICOs became a funding machine.

A 2018 study examined 1,388 ICOs published by the end of 2017, showing how crowded the cycle became.

Stablecoins, custody, exchanges, on-chain settlement, DeFi niches, tokenized speculation rails.

Most utility tokens, decentralized Uber/Airbnb clones, governance theater, enterprise blockchain pilots.

Voice would become the next major computing interface.

Alexa and Google Home spread quickly through homes, and every brand imagined voice commerce and voice apps.

TechCrunch reported smart speakers reached critical mass in 2018, citing U.S. ownership around 41%.

Timers, music, smart-home control, dictation, voice UI primitives, wake-word hardware.

Voice shopping, rich third-party voice apps, smart speakers as a broad software platform.

New networks would unlock AR, autonomous vehicles, remote surgery and edge computing.

Spectrum auctions, carrier marketing, geopolitical fights over telecom equipment and handset upgrades made 5G unavoidable.

Axios warned in June 2019 that 5G mania had swept the industry while business cases were still unclear.

Network upgrades, fixed wireless access, better mobile bandwidth, private networks, industrial connectivity niches.

Near-term killer apps, consumer willingness to pay more, remote-surgery futurism, citywide mmWave assumptions.

Blank-check companies would become a faster, better route for tech companies to go public.

Low rates, retail trading, celebrity sponsors and late-stage startup valuations turned SPACs into a tech-finance frenzy.

CNBC reported U.S. SPAC fundraising hit $87.9B in the first three months of 2021, already exceeding all of 2020.

Some public listings, alternative IPO pressure, better understanding of late-stage liquidity risks.

Most hype valuations, celebrity sponsors, EV/space/deep-tech projections, SPACs as default startup exit.

Everyone could monetize an audience directly and escape platform dependence.

Pandemic internet use, TikTok, Substack, Patreon, Clubhouse and creator funds made individual media businesses look venture-scale.

Axios reported VCs plowing money into creator startups as Patreon raised $155M at a $4B valuation in April 2021.

Newsletter platforms, paid communities, creator tools, affiliate commerce, vertical media businesses.

Creator middle-class inevitability, audio-social clones, many creator SaaS tools without retention.

Tokenized ownership would reinvent art, collectibles, gaming, identity and media.

Crypto wealth, profile pictures, marketplaces, celebrity drops and Discord communities made NFTs feel like consumer crypto's breakout app.

Chainalysis reported NFT marketplace value sent fell from $3.9B in the week of February 13, 2022 to $964M by March 13.

Digital provenance, loyalty mechanics, tickets, game assets in constrained ecosystems, collector niches.

The broad JPEG asset-class thesis, celebrity drops, most PFP projects, metaverse-land speculation.

Persistent 3D worlds would become the next internet, office and social platform.

Facebook renamed itself Meta in October 2021 and made the metaverse the center of its corporate narrative.

Meta reported Reality Labs losses of $10.2B for 2021 and $13.7B for 2022 while the consumer platform thesis failed to normalize.

Game engines, simulation, VR niches, spatial computing, training environments, 3D design workflows.

The mass social metaverse, VR office default, virtual land boom, avatar-workplace inevitability.

Foundation models would make text, code, images, audio and video programmable.

ChatGPT turned frontier language models into a mass consumer interface and made AI legible to non-specialists.

ChatGPT launched November 30, 2022 and reached an estimated 100M monthly users within about two months.

Coding assistants, chat interfaces, RAG, multimodal models, AI search, synthetic media, enterprise copilots.

Wrapper apps without distribution, prompt-framework cargo cults, many undifferentiated AI SaaS tools.

Models would stop answering and start doing multi-step work.

Tool use, coding agents, computer-use demos and enterprise automation pushed attention from chat to delegated workflows.

McKinsey's 2025 AI survey reported 23% of respondents scaling agentic AI somewhere and another 39% experimenting.

Coding agents, research agents, service-desk automation, workflow orchestration, guardrail/guardian layers.

Fully autonomous employee replacement demos, brittle browser agents, agent-washing of ordinary chatbots.

AI would leave the browser and do useful work in factories, warehouses, roads and skies.

Foundation models, better perception, cheaper sensors, drones, humanoid demos and labor scarcity converged into physical AI.

IFR reported 542,000 industrial robots installed in 2024, more than double the number from ten years earlier.

Manufacturing automation, drones, inspection, logistics robots, cobots, robot fleet software.

Near-term home general-purpose servants, humanoid demo inflation, robots without measurable uptime or ROI.

New compute physics would break current limits in cryptography, chemistry and optimization.

Government funding, cloud access, lab milestones and the word quantum make the field sound like the next compute platform.

McKinsey's 2025 tech outlook frames quantum as transformative in specific domains but requiring more advances for practical business impact.

Research, national capability, cryptography transition, chemistry/materials partnerships, specialist cloud access.

The broad near-term platform narrative for ordinary developers and enterprises.